Table of Contents

What is an Owner Contribution?

When a business is first starting out, its owners or co-founders may need to invest their own money in the company in order to fund its operations. This type of investment, known as capital investment, is essential for the business to have the resources it needs to grow and develop. Capital investments can be used to purchase equipment, pay for marketing efforts, hire additional staff, and cover other expenses.

It is important for a business to accurately account for capital investments made by its owners or shareholders. This involves recording the investments in the company’s financial records and tracking them separately from other types of income or expenses. Accurately accounting for capital investments helps to ensure that the company’s financial statements are accurate and up to date, and it helps to prevent misunderstandings or disputes between the owners and the business.

In addition to recording capital investments as an asset in the company’s financial statements, it is also important to recognize any money that must be repaid to the owners as a liability. This helps to ensure that the business is transparent about its financial obligations and helps to prevent misunderstandings or disputes in the future. Overall, accurately accounting for capital investments is an essential part of good financial management for any business.

Journal Entries for Owner Contribution to Business

Journal entry for shareholder contribution to a corporation

When a corporation is first starting out, it may need to rely on its shareholders for funding in order to pay its employees, suppliers, and other expenses. This initial injection of funds is often necessary to get the corporation up and running and to purchase the assets and inventory it needs to operate.

There are two main methods by which this initial injection of funds can be accounted for:

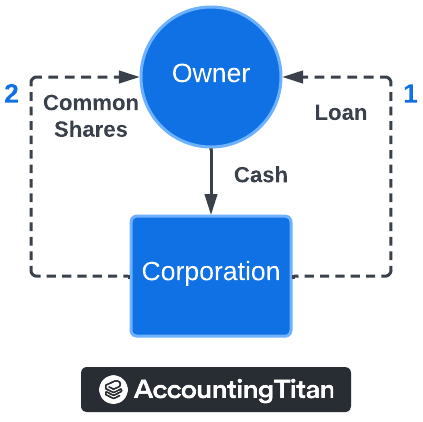

- Shareholder loan method: The corporation can record the initial injection of funds as a loan from the shareholder. In this case, the corporation would record a liability on its balance sheet to reflect the amount of the loan and the shareholder would be entitled to interest on the loan. This method is typically used when the corporation is an established business with revenues and profits, and the shareholder expects to be repaid the loan with interest.

- Share capital method: The shareholder provides an initial injection of funds to a newly formed corporation, and the corporation issues additional shares of stock to the shareholder in exchange for the funds. The value of the shares issued is equal to the amount of the funds injected, and the shareholder becomes a shareholder of the corporation with an ownership stake based on the number of shares they hold. This method of accounting for an initial injection of funds is commonly used when the corporation is a start-up and does not yet have any revenue or profits.

Both of these methods are acceptable ways to account for an initial injection of funds from a shareholder to a corporation. The method chosen will depend on the specific circumstances of the transaction and the expectations of the shareholder.

Shareholder loan method

Example: James Nguyen, a majority shareholder of Fresh Spa Inc., has invested $500,000 to fund the corporation’s payroll for the next 3 months. He expects to be repaid in 4 months when the corporation is expected to have generated sufficient revenues to fund the loan repayment.

| Account | ||

|---|---|---|

| Cash | $500,000 | |

| Due to/from shareholder | $500,000 |

Share capital method

Example: James Nguyen, a majority shareholder of Fresh Spa Inc., has invested $500,000 to fund the corporation’s payroll for the next 3 months. He does not expect immediate repayment and would like to take back 500 common shares of Fresh Spa Inc. in exchange for the cash infusion.

| Account | ||

|---|---|---|

| Cash | $500,000 | |

| Common shares | $500,000 |

Journal entry for owner contribution to a sole proprietorship

A sole proprietorship is a type of business that is owned and operated by a single individual. It is the most basic form of business structure and is relatively easy to set up and maintain. When the owner of a sole proprietorship contributes cash or assets to the business, these contributions are recorded in the company’s financial records by debiting the Cash or Assets accounts and crediting the Owner’s Investment account. This helps to accurately track the owner’s contributions and ensure that the business’s financial statements are accurate and up to date.

Example

John Smith, a lawyer, contributed $150,000 to his sole proprietorship business through which he provides legal services to individuals. The $150,000 will be used to pay rent and law clerks.

| Account | ||

|---|---|---|

| Cash | $150,000 | |

| Owner’s investment | $150,000 |