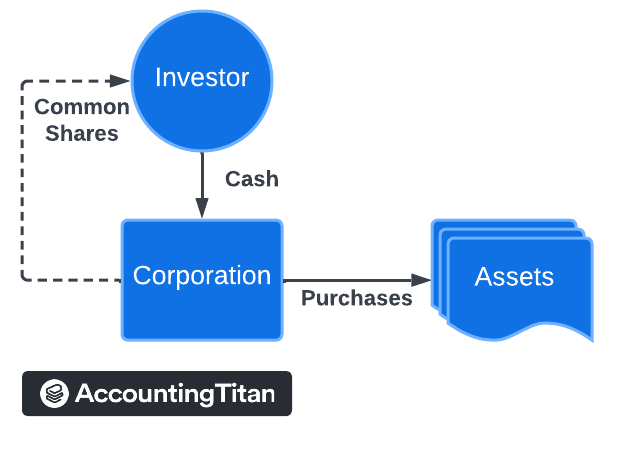

Selling common shares to investors is a common method for companies to raise capital. This capital is used by the company to fund operations, invest in assets, and pay salaries. When a company issues common shares, it is selling ownership in the company to investors in exchange for cash. These investors then become shareholders, and their ownership stake in the company is based on the percentage of shares they hold. Issuing share capital allows companies to raise the funds they need to grow and develop.

Table of Contents

What are common shares?

Common shares are a form of ownership of a corporation. Common shares represent an equity share in a corporation with the rights to vote on the election of the board of directors and major decisions, receive dividends if declared by the board of directors, and benefit from any remaining proceeds of liquidation if the company is dissolved, after debtholders, bondholders, and preferred shareholders.

Common shares may also be referred to as common stock, ordinary shares, junior equity, or voting shares.

Common shares represent an asset to the holder of the shares (the owner of the common shares) and are classified as equity on the corporation which issued the common shares.

Journal entries for the issuance of common shares

When a company raises capital from investors, it does so by issuing securities, which are financial instruments that represent ownership in the company or the right to receive a future financial benefit. Common shares are one type of security that companies may issue to raise capital.

Common shares represent ownership in a company, and holders of common shares are entitled to a share of the company’s profits and assets. When a company issues common shares, it is effectively selling ownership stakes in the company to the investors who purchase the shares.

When a company issues new common shares from treasury, it means that the company is creating and selling new shares that have not previously been outstanding. Treasury shares are authorized but not currently owned by anyone, so they are effectively “new” shares that the company is creating and selling to raise capital.

Journal entry for the issuance of common shares without par value

Common shares without par value are journalized by debiting cash (asset) for the amount received for the shares and crediting common shares (equity) for the same amount.

For example, if Oscorp Inc. sells 50 common shares for $1,000 each to Stark Industries Inc., it would be accounted for by Oscorp Inc. as such:

| Account | ||

|---|---|---|

| Cash | $50,000 | |

| Common shares | $50,000 |

Journal entry for the issuance of common shares with par value

Common shares with par value are journalized by debiting cash (asset) for the amount received for the shares and crediting common shares (equity) up to the par value, with the balance of the entry credited to additional paid-in capital (equity).

For example, if Oscorp Inc.’s common shares have a par value of $100 per share, and the company sells 50 common shares for $1,000 each to Stark Industries Inc., it would be accounted for by Oscorp Inc. as such:

| Account | ||

|---|---|---|

| Cash | $50,000 | |

| Common shares | $5,000 | |

| Additional paid-in capital | $45,000 |

In the example above, the additional paid-in capital of $45,000 is calculated by the selling price of the 50 common shares of $50,000 (50 shares x $1,000 per share), minus the par value of the 50 common shares of $5,000 (50 shares x $100 par value).